Can Intel 18A Challenge AMD’s CPU Leadership?

For much of the past decade, Intel has watched AMD steadily erode its dominance across both consumer and enterprise CPU markets. What was once a near-monopoly in x86 computing has evolved into a highly competitive landscape where AMD’s Ryzen and EPYC product lines have become formidable alternatives.

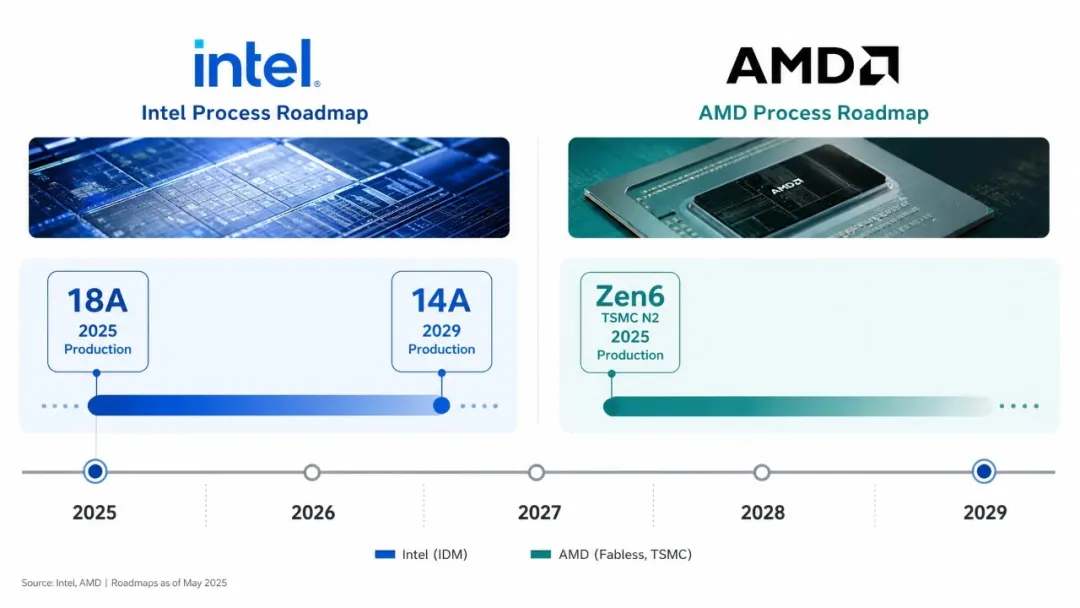

Intel’s answer to this challenge is its ambitious 18A manufacturing node. More than just another process shrink, 18A represents a fundamental technological reset for the company. Its success—or failure—could determine Intel’s competitive position for the next decade.

The stakes extend far beyond benchmark charts. Enterprise purchasing decisions, cloud infrastructure investments, and consumer upgrade cycles may all be influenced by the outcome of Intel’s 18A strategy.

🚀 18A: Intel’s Most Important Process Node in a Decade #

Intel’s current position is the result of several overlapping challenges that accumulated over the past ten years:

- Delays in manufacturing node transitions

- Architectural roadmap disruptions

- Packaging and product schedule setbacks

- Increased competition from TSMC-powered AMD products

While Intel struggled to maintain execution consistency, AMD capitalized on the opportunity through:

- A disciplined Zen architecture roadmap

- Aggressive adoption of advanced TSMC process technologies

- Early and successful deployment of chiplet-based designs

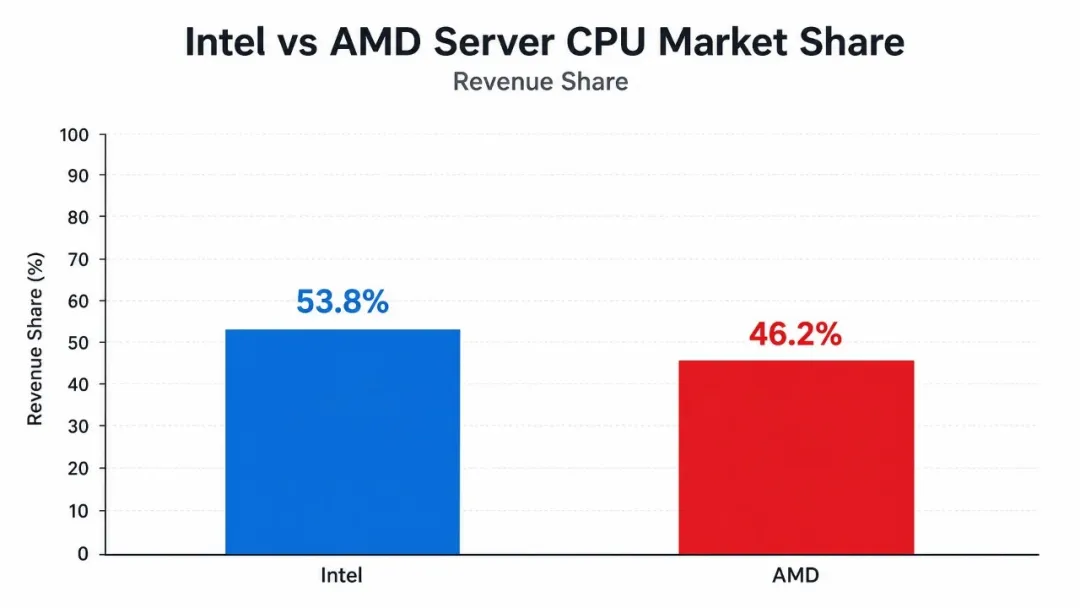

The result has been remarkable growth across both desktop and server segments. AMD has become a preferred platform among enthusiasts and has captured a significant share of enterprise deployments, with server revenue approaching parity with Intel in many segments.

Against this backdrop, Intel has positioned 18A as its defining comeback technology.

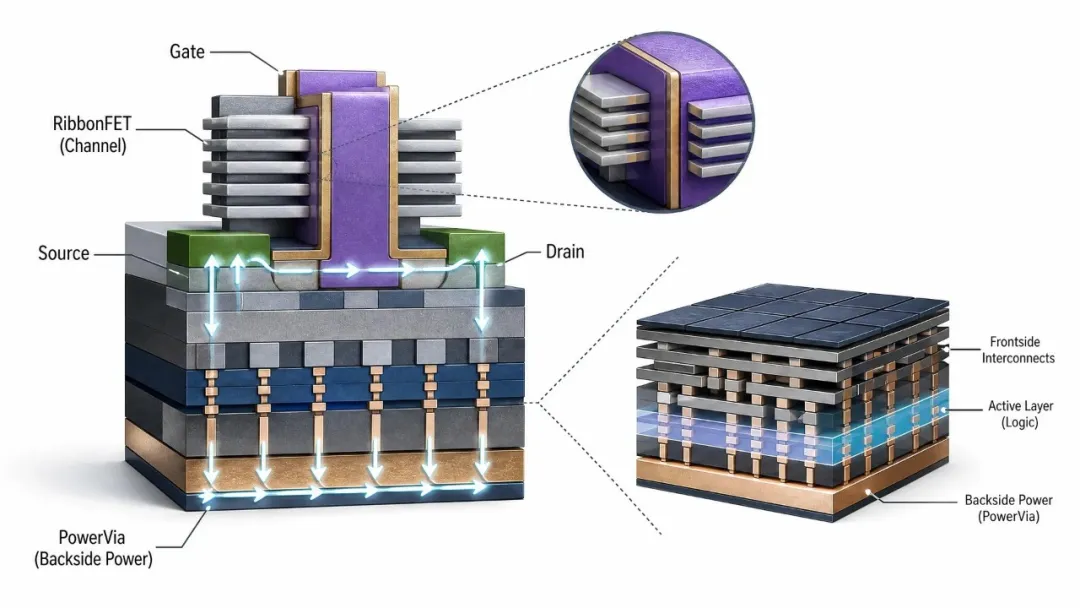

RibbonFET: Intel’s Gate-All-Around Transition #

The first major innovation in 18A is RibbonFET, Intel’s implementation of Gate-All-Around (GAA) transistor technology.

Traditional FinFET transistors have powered semiconductor scaling for years, but they are approaching physical limitations as geometries continue shrinking. RibbonFET addresses these challenges by surrounding the transistor channel on all sides, improving electrostatic control and reducing leakage current.

Potential benefits include:

- Higher performance at similar power levels

- Improved energy efficiency

- Better scalability for future nodes

- Reduced leakage in dense designs

The industry broadly views GAA transistors as the next major step in transistor evolution, and Intel’s adoption of RibbonFET marks a significant architectural milestone.

PowerVia: Rethinking Power Delivery #

The second pillar of 18A is PowerVia, Intel’s backside power delivery technology.

Traditionally, both signal routing and power distribution occupy the same metal layers above the transistor structures. As transistor density increases, competition for routing resources becomes a major bottleneck.

PowerVia addresses this by moving power delivery to the backside of the wafer.

Benefits include:

- Reduced signal congestion

- Improved power integrity

- Enhanced routing efficiency

- Greater performance scalability

This approach allows front-side interconnect layers to focus primarily on data movement, potentially enabling more efficient and higher-performing designs.

Claimed Performance Improvements #

Compared with Intel 3, Intel projects that 18A can deliver:

- Up to 15% better performance-per-watt

- Approximately 30% higher transistor density

- Improved efficiency under AI and compute-intensive workloads

If these targets are achieved in production silicon, 18A would represent Intel’s most meaningful process advancement in years.

💻 Panther Lake: The Consumer Market Test #

The first major client platform based on 18A will be Panther Lake.

Panther Lake carries substantial importance because it serves as the public proof point for Intel’s manufacturing recovery. Consumers, OEMs, and investors will closely examine:

- Performance gains

- Power efficiency

- Thermal characteristics

- Manufacturing yields

- Product availability

Why the Client Market Matters #

The consumer market provides an ideal environment for Intel to demonstrate the strengths of 18A.

Key advantages include:

- High shipment volumes

- Strong OEM relationships

- Faster product adoption cycles

- Less stringent validation requirements than enterprise deployments

If Panther Lake delivers meaningful battery-life improvements, stronger integrated AI acceleration, and competitive performance, Intel could regain momentum in premium notebooks and mainstream desktops.

However, success in consumer PCs does not automatically translate into success in data centers.

🏢 Clearwater Forest: The Real Strategic Battlefield #

While Panther Lake will attract headlines, Clearwater Forest may ultimately determine whether 18A changes Intel’s competitive position.

The server market has become one of AMD’s greatest success stories. EPYC processors have steadily expanded their presence in:

- Cloud infrastructure

- Enterprise data centers

- High-performance computing

- AI training environments

Unlike consumer buyers, enterprise customers prioritize:

- Total cost of ownership

- Platform stability

- Performance-per-watt

- Long-term roadmap confidence

- Software ecosystem maturity

Winning back these customers requires more than a fast processor.

Challenges Facing Intel in Servers #

Intel must overcome several hurdles:

Rebuilding Trust #

Many enterprises shifted toward AMD after years of observing Intel roadmap delays.

Even if Clearwater Forest is technically competitive, some organizations may wait multiple generations before making major platform transitions.

Efficiency Expectations #

Modern data centers increasingly optimize around power consumption.

A modest performance advantage is no longer enough if it comes with significantly higher energy costs.

AI Infrastructure Competition #

The rise of AI has shifted purchasing priorities.

Organizations now evaluate CPUs alongside:

- GPUs

- AI accelerators

- Networking platforms

- Memory architectures

Intel must demonstrate how 18A-based processors fit into these evolving infrastructures.

📈 Different Markets, Different Opportunities #

The difficulty of reclaiming market share varies significantly by segment.

Consumer Desktop #

This remains one of the most accessible opportunities for Intel.

Many users still purchase based on:

- Gaming performance

- Brand familiarity

- Retail availability

- Platform pricing

A strong Panther Lake launch could quickly improve Intel’s position among mainstream consumers.

Mobile Computing #

Notebook systems represent another promising area.

Power efficiency improvements from RibbonFET and PowerVia could allow Intel to compete more aggressively against:

- AMD Ryzen mobile processors

- Arm-based Windows systems

- Apple’s Apple Silicon ecosystem

Enterprise Servers #

This is the most difficult battleground.

AMD’s EPYC platform has established a strong reputation for:

- Core density

- Energy efficiency

- Platform consistency

Intel must not only match these advantages but also convince customers to reverse infrastructure strategies that have been years in the making.

🔬 Manufacturing Success Matters as Much as Architecture #

One critical factor often overlooked in discussions about 18A is manufacturing execution.

Even the most advanced architecture cannot succeed without:

- High production yields

- Stable supply chains

- Predictable ramp schedules

- Competitive manufacturing costs

Intel’s ability to deliver 18A at scale may ultimately be more important than the technical specifications themselves.

A successful ramp would validate Intel’s broader foundry strategy and reinforce confidence in future nodes. Conversely, production setbacks could undermine even impressive architectural achievements.

🎯 Can 18A Reverse AMD’s Momentum? #

The answer depends on how success is defined.

If the goal is to immediately restore Intel’s historic dominance, 18A alone is unlikely to achieve that. AMD’s current position is the result of more than a decade of disciplined execution, and market leadership is not easily reclaimed.

However, if the objective is to reestablish technological competitiveness and halt AMD’s market-share gains, 18A has the potential to be a turning point.

RibbonFET and PowerVia represent genuine innovations rather than incremental refinements. Combined with products such as Panther Lake and Clearwater Forest, they provide Intel with a credible path back into direct competition at the leading edge.

🏁 Conclusion #

Intel’s 18A node is far more than a manufacturing milestone—it is the cornerstone of the company’s broader recovery strategy.

With RibbonFET and PowerVia introducing fundamental changes to transistor and power-delivery architecture, 18A represents Intel’s most ambitious technological leap in over a decade. Panther Lake will test its appeal in consumer markets, while Clearwater Forest will determine whether Intel can regain relevance in modern data centers.

The ultimate question is not whether 18A can outperform a specific AMD product. Rather, it is whether Intel can consistently execute on a long-term roadmap, deliver products on schedule, and rebuild the confidence of customers who have increasingly embraced alternatives.

If Intel succeeds, the x86 market could enter a new phase of intense competition. If it falls short, AMD’s momentum may continue well into the next decade.